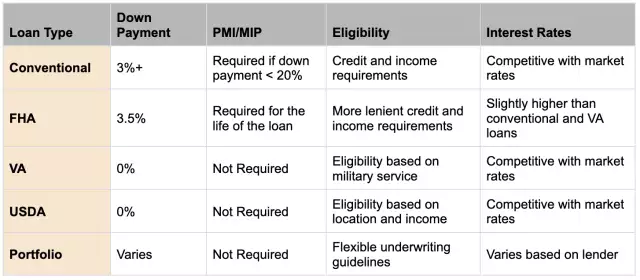

Navigating the World of Jumbo Loans: What Homebuyers Need to Know

A jumbo loan is a type of mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). These loans are designed for homebuyers who are looking to purchase a high-end property or a home in a high-cost area. In this blog post, we'll take a closer look at jumbo loans and what homebuyers need to know about this loan type.

First, it's important to understand that jumbo loans typically have stricter credit and income requirements than conforming loans. This is because jumbo loans are considered to be higher risk than conforming loans. As a result, borrowers will generally need a higher credit score and a lower debt-to-income ratio to qualify for a jumbo loan.

Another key difference between jumbo loans and conforming loans is the down payment requirement. Jumbo loans typically require a larger down payment, typically around 20-25% of the purchase price. This is because jumbo loans are considered to be higher risk and lenders want to ensure that borrowers have a significant amount of equity in the property.

Jumbo loans also typically have higher interest rates than conforming loans. This is because they are considered to be higher risk and lenders charge a higher rate to offset this risk. However, borrowers may be able to negotiate a lower rate if they have a strong credit score and a low debt-to-income ratio.

Let's take an example of a person, Alex, who wants to buy a $1,000,000 property and he has a good credit score and a stable income. In this case, Alex can qualify for a jumbo loan with a 25% down payment of $250,000 and an interest rate of 4%. His monthly payment would be around $4,500 including principal, interest, taxes, and insurance.

Pros and Cons of Lumbo Loans

Pros of Jumbo Loans

- Higher loan limits: Jumbo loans allow borrowers to purchase high-end properties or homes in high-cost areas that may not be possible with conforming loans.

- Flexible terms: Jumbo loans may offer more flexible terms and options compared to conforming loans, such as adjustable-rate mortgages (ARMs) or interest-only options.

- Lower mortgage insurance: Unlike conforming loans, Jumbo loans may not require mortgage insurance for borrowers who make a large down payment.

- Lower interest rates: Some borrowers with excellent credit, high income, and low debt-to-income ratios may be able to qualify for lower interest rates on Jumbo loans.

Cons of Jumbo Loans

- Higher down payment requirement: Jumbo loans typically require a higher down payment, typically around 20-25% of the purchase price, which can be a significant financial burden for some borrowers.

- Higher interest rates: Jumbo loans are considered to be higher risk than conforming loans and as a result, they may have higher interest rates.

- Strict credit and income requirements: Borrowers may need a higher credit score and a lower debt-to-income ratio to qualify for a Jumbo loan, which can make it more difficult for some borrowers to qualify.

- Limited availability: Jumbo loans may not be available from all lenders, which can make it more difficult to find a lender that offers this type of loan.

- Limited loan options: Jumbo loans may not have the same variety of loan options as conforming loans, such as government-backed loans or special programs for first-time homebuyers.

Jumbo loans: Who should apply and who should avoid them

Who should consider Jumbo Loans

- High-income earners: Borrowers with high income and strong financial assets may be able to afford the higher down payment and interest rates associated with Jumbo loans.

- Homebuyers in high-cost areas: Borrowers looking to purchase a home in a high-cost area may need a Jumbo loan to finance the purchase.

- High-end property buyers: Borrowers looking to purchase a high-end property, such as a luxury home or waterfront property, may need a Jumbo loan to finance the purchase.

- Borrowers with good credit: Borrowers with good credit, low debt-to-income ratio and a stable income, may be able to qualify for lower interest rates on Jumbo loans.

Who should avoid Jumbo Loans

- Low-income earners: Borrowers with low income may struggle to afford the higher down payment and interest rates associated with Jumbo loans.

- Homebuyers in low-cost areas: Borrowers looking to purchase a home in a low-cost area may not need a Jumbo loan and may be better off with a conforming loan.

- Borrowers with poor credit: Borrowers with poor credit may struggle to qualify for a Jumbo loan and may be better off with a conforming loan or working on improving their credit score.

- Borrowers with high debt-to-income ratio: Borrowers with high debt-to-income ratio may not qualify for a Jumbo loan and may be better off with a conforming loan or working on paying off some of their debts.

- Borrowers who plan to move soon: Borrowers who plan to move soon may not want to take on a Jumbo loan with a long-term commitment, instead, they may prefer a conforming loan or an adjustable-rate mortgage (ARM) with a shorter term.

Frequently Asked Questions about Jumbo Loans

What is the maximum loan amount for a Jumbo loan?

-The maximum loan amount for a Jumbo loan can vary depending on the location and the lender, but it typically ranges between $510,400 and $3,000,000.

Do I need a higher credit score for a Jumbo loan?

-Yes, borrowers typically need a higher credit score to qualify for a Jumbo loan compared to a conforming loan.

What is the down payment requirement for a Jumbo loan?

-The down payment requirement for a Jumbo loan is typically around 20-25% of the purchase price.

Are the interest rates higher for Jumbo loans?

Yes, interest rates are typically higher for Jumbo loans as they are considered to be higher risk than conforming loans.

In conclusion, jumbo loans are designed for homebuyers who are looking to purchase a high-end property or a home in a high-cost area. These loans typically have stricter credit and income requirements, a larger down payment requirement and higher interest rates than conforming loans. It's important for homebuyers to understand these requirements and factor them into their budget and affordability.