From Fair Housing to TILA/RESPA: Understanding the Compliance Requirements in Mortgage Marketing

From Fair Housing to TILA/RESPA: Understanding the Compliance Requirements in Mortgage Marketing

The mortgage industry is heavily regulated, and compliance is essential for lenders, brokers, and other financial institutions. In this blog post, we'll take a closer look at two key areas of concern in mortgage marketing: the Fair Housing Act (FHA) and the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA). We'll explain what these laws are, what they require, and give some examples to help you understand how they apply to your business.

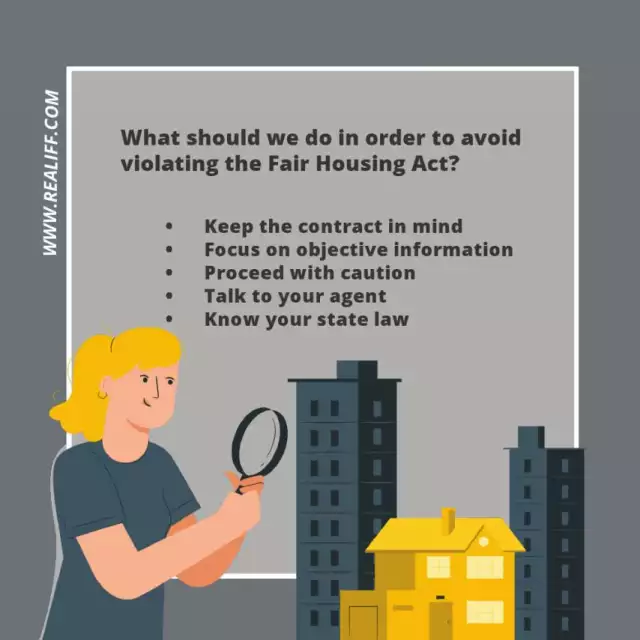

The Fair Housing Act (FHA)

The Fair Housing Act (FHA) prohibits discrimination on the basis of race, color, national origin, religion, sex, familial status, or disability in the sale, rental, or financing of housing. In the mortgage industry, this means that lenders and brokers must ensure that their advertising and marketing materials do not contain any discriminatory language or imagery. They must also ensure that their loan products and services are available to all borrowers, regardless of their protected status.

TILA and RESPA

The Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA) are federal laws that are designed to protect borrowers by requiring lenders and brokers to disclose certain information and prohibiting certain practices that can lead to higher costs for borrowers. Under TILA, lenders must provide borrowers with a "truth-in-lending" disclosure that includes the terms of the loan, the interest rate, and the fees associated with the loan. Under RESPA, lenders and brokers are prohibited from engaging in certain practices, such as kickbacks and referral fees, that can lead to higher costs for borrowers.

Compliance in Advertising and Marketing

To ensure compliance with the FHA, lenders and brokers should develop and implement policies and procedures for their advertising and marketing activities. This includes reviewing all advertising and marketing materials for discriminatory language or imagery, and ensuring that all loan products and services are available to all borrowers regardless of their protected status.

Compliance in Loan Origination

To ensure compliance with TILA and RESPA, lenders should provide borrowers with the required disclosures and ensure that they are accurate and complete. Lenders should also train their loan originators on these requirements and conduct regular audits to ensure compliance.

Penalties for non-compliance

Non-compliance with FHA, TILA, and RESPA can lead to significant penalties for lenders and brokers, including fines, penalties, and reputational damage. It's important that lenders and brokers are aware of these penalties and take steps to ensure compliance with these laws.

Examples of Compliance

- A lender should not advertise "no minorities" or "whites only" in their advertisement.

- A lender should not charge a higher interest rate to a borrower based on their protected status

- A lender should not give referral fee to real estate agent for sending business their way

- A lender must provide borrowers with a "good faith estimate" of closing costs at the time of loan application and a HUD-1 Settlement Statement at closing.

- A lender should not charge an application fee before providing the applicant with a "truth in lending" disclosure

- A lender should not charge a prepayment penalty fee, this is prohibited by TILA

Frequently Asked Questions (FAQs) about Compliance Requirements in Mortgage Marketing

Q: What is the Fair Housing Act (FHA)?

A: The Fair Housing Act (FHA) is a federal law that prohibits discrimination on the basis of race, color, national origin, religion, sex, familial status, or disability in the sale, rental, or financing of housing. This includes advertising and marketing materials, as well as loan products and services.

Q: What is TILA and RESPA?

A: The Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA) are federal laws that are designed to protect borrowers by requiring lenders and brokers to disclose certain information and prohibiting certain practices that can lead to higher costs for borrowers. TILA requires lenders to provide borrowers with a "truth-in-lending" disclosure that includes the terms of the loan, the interest rate, and the fees associated with the loan. RESPA prohibits lenders and brokers from engaging in certain practices, such as kickbacks and referral fees, that can lead to higher costs for borrowers.

Q: What are some examples of discriminatory language or imagery in advertising and marketing materials?

A: Examples of discriminatory language or imagery in advertising and marketing materials include "no minorities" or "whites only" in an advertisement, or using imagery that suggests a preference for certain protected groups.

Q: What are some examples of prohibited practices under TILA and RESPA?

A: Examples of prohibited practices under TILA and RESPA include charging a higher interest rate to a borrower based on their protected status, giving referral fees to real estate agents for sending business their way, charging application fees before providing the applicant with a "truth in lending" disclosure, charging a prepayment penalty fee and not providing a "good faith estimate" of closing costs at the time of loan application and a HUD-1 Settlement Statement at closing.

Q: What are the penalties for non-compliance with FHA, TILA, and RESPA?

A: Penalties for non-compliance with FHA, TILA, and RESPA can include fines, penalties, and reputational damage.

Q: What steps should lenders and brokers take to ensure compliance with FHA, TILA, and RESPA?

A: Lenders and brokers should develop and implement policies and procedures for their advertising and marketing activities, train their employees on these policies and procedures, conduct regular audits to ensure compliance and work with compliance experts and legal counsel to stay up-to-date on the latest regulations and industry best practices.

In conclusion, compliance with the Fair Housing Act (FHA), the Truth in Lending Act (TILA), and the Real Estate Settlement Procedures Act (RESPA) is essential for lenders, brokers, and other financial institutions. With the right policies and procedures in place, they can ensure that their advertising and marketing efforts are in compliance with all applicable laws and regulations, while still reaching and serving their target borrowers. It's important for lenders and brokers to stay informed about the latest regulations and industry best practices, and to work with compliance experts and legal counsel to ensure that their business is in compliance with all applicable laws. Remember that non-compliance can lead to significant penalties and reputational damage, so it's crucial to take compliance seriously. By understanding and implementing the compliance requirements, lenders and brokers can ensure that their marketing and advertising efforts are fair and transparent, and that they are serving the best interests of their borrowers.

Here are some related topics

- Fair lending practices and compliance

- Mortgage industry regulations and laws

- Advertising and marketing compliance in the mortgage industry

- TILA and RESPA compliance for lenders

- Fair Housing Act and discrimination in the mortgage industry

- Mortgage compliance risk management

- Best practices for compliance in the mortgage industry

- Compliance training for mortgage industry professionals

- Penalties for non-compliance in the mortgage industry

- The impact of technology on compliance in the mortgage industry.