0 Followers

728 Views

Levelset

0 Followers

728 Views

67

Posts

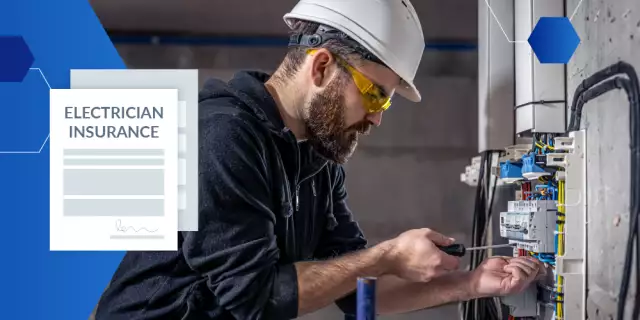

Insurance for Electricians: What It Covers & Why You May Need It

At any given time, an electrician could be performing work on a construction project that involves high stakes. For example, a faulty connection somewhere along a circuit could trigger a fire that causes significant damage or total loss to the structure. This type of damage may leave electrical contractors unable to foot the bill.

How a Construction-to-Permanent Loan Impacts Contractors & Lenders

A construction-to-permanent loan can help owners save time and money — one loan and closing transaction streamlines. When a property owner wants to finance the construction of a new building, they typically have to obtain two loans: one loan for the mortgage on the completed home, and another for the land purchase and construction expenditures.

17 Alternatives to Common Building Materials

If necessity is the mother of invention, consider scarcity and inflation the grandparents of throwing your hands in the air and saying "Well, what can I order?" In recent years, material shortages and volatile material prices have slowed so many projects to a grinding halt. As a result, contractors and property owners are increasingly considering [] The post 17 Alternatives to Common Building Materials appeared first on Levelset.

A Plumbing Contractor’s Guide to Insurance Coverage

Plumbing contractors should include business insurance as an integral part of their financial strategy. When you tackle the jobs you’ve secured, it’s also important to plan for the unexpected. With numerous policies available, the plumbing contractor’s insurance landscape offers many ways for you to protect your physical and financial business assets. Obtaining an insurance policy […]

The post A

... more

What Is a Certificate of Insurance (COI) for Contractors — and When Do You Need One?

Contractor's insurance should be a crucial part of your financial strategy. Insurance also puts other parties’ minds at ease when they want to hire you as a specialty contractor. Before you can get hired and begin work, you’ll need to prove to owners and/or general contractors that you are a special contractor.

How to Increase Cash Flow for Your Construction Business When You Can’t Get the Financing You Need From the Bank

As a commercial specialty contractor, it can be frustrating to have the crew, time, and skills you need to take on construction projects but not enough cash to purchase materials. Many contractors feel using their personal accounts is the only way to get the cash they need to help their business and start bidding on jobs. In this article, we’ll share five ways you can increase your cash flow.

Job Safety Analysis (JSA): What It Is and How to Do It

A job safety analysis (JSA) is an analysis of job tasks that seeks to identify hazards before they occur. The maximum federal OSHA penalty for violations can be up to $14,502 per violation. The benefits of JSAs can help contractors avoid fines and fines. For each task, JSAs also reduce workers compensation insurance premiums, saving contractors money and increasing profits. The goal in performing a JSA is Document the answers to these questions.

Completed Operations: A Contractor’s Guide to Coverage, Cost, & More

Completed operations insurance covers property damage or injury caused by work that a contractor performed in the past. It pays for repairs of damages to the surrounding property, as well as legal expenses incurred during a lawsuit. Completed operations coverage lasts for a period of 10 years. The law of repose for most states has a 10-year limit on damages. The statute of reposed for most for most states is 10 years and is not out. For most.

What is Equipment Floater Insurance for Contractors?

An equipment floater offers insurance protection for your business property as it moves from location to location. This type of coverage is part of the broader category known as inland marine insurance. As a contractor, you likely have a considerable amount of money sunk into tools of the trade. Most construction subcontractors own some specialized business property and spend time moving from job to job. You can secure a wide spectrum of coverage. An all-risk policy would give you the broadest protection.

CCIP & OCIP: A Guide to Controlled Insurance Programs in Construction

A Controlled Insurance Program (CIP) is an insurance package

designed to cover all liability and losses during an entire

construction project. The cost of the premiums will also be

affected by the amount of the deductible, and whether the policy

includes self-insured retention (SIR) The deductible on a CIP

policy works the same as any other insurance policy. ‘The insurance

is truly excess,’ says Joshua Rogove. “The insurance are truly

excess of the SIR,” says JoshuaRogove. The sponsor can purchase the... more

9 Tips for Starting an Architecture Firm

Most architects start their own firms because they want to spend

more time being creative and expressing their design ideas.

Architectural firms need to monitor the cash coming in and going

out of the business to ensure they have enough on hand to cover

critical expenses. Staggering design and administrative software

expenses so they don’t all fall at the same time can help to reduce

cash flow problems. If all your subscriptions fall in the same

month, you can take quite a cash hit. You may be tempted to bill... more

A Cash Flow Guide for Architects

A cash flow statement analyzes the cash transactions within a given time period. An hourly rate works best for projects where the entire scope is not clear. The Breakeven Rate is calculated as total operating expenses is divided by direct labor expenses. For custom residential design, Gray recommends 8% to 15% of the cost of the project as the design fee.

Overcoming Construction Labor Shortages to Grow Your Business

Construction is booming, so more workers are needed to help meet

the industry's high labor demands. Many construction companies

struggle to find and retain a top-notch labor force. The

construction labor shortage and escalating inflation are causing

stress and working capital difficulties for specialty contractors.

While labor shortages may seem like a people problem, they're a

cash flow issue too. So how are construction companies overcoming

these labor shortage challenges? Polanco Business Solutions CEO

Alberto... more

How to Start an Electrical Business: 9 Tips for Growth

The US electrical industry has more than 1 million employees

working for 200,000 businesses. In order to grow, an electrician

company must proactively manage cash flow - or you will end up

doing as well as a frayed wire. If your business is cash flow

negative, it doesn’t matter if you have significant revenue coming

in down the line. Growing and maintaining your electrical business

means having positive cash flow means having good cash flow to

expand your workforce and take on new jobs. Your profit is to

expand... more

How to Get Paid on Oregon Public Projects

Though popular thinking is often that public projects run into

fewer payment problems than private ones do, that's a

misconception: Even when public works projects are a major source

of benefit, contractors are at just as much risk of slow payment or

nonpayment as on any private project. Payment protection on Oregon

public projects Even though payment challenges can be remarkably

similar, payment protection is very different between private and

public work. Oregon prompt payment laws Prompt payment laws

regulate... more

Does a Lien Affect Your Credit Score?

Mechanics liens are different from other collection instruments, so they are treated differently when it comes to reporting on your credit history. Liens are available in all 50 states and are included in each state’s laws (and in some cases, the state constitution) Each state has different rules that govern the lien filing process, including notice requirements, filingdeadlines, and expiration dates. If a contractor doesn’t follow the rules, their mechanics lien. The lien may be invalid.