1 Follower

862 Views

Better

1 Follower

862 Views

48

Posts

How to Get to Know Your Neighborhood | Better Mortgage

Moving to a new house brings a lot of memorable "Firsts": the first

time you walk through the door as an owner, the first meal you cook

in your new kitchen, and the first holiday you'll celebrate in your

new living space. One of the best ways to feel settled in again is

to get to know your new neighborhood. Try new things Grab a fanny

pack and a selfie stick: It's time to be a tourist for a day! Check

out local hot spots, like museums, art galleries, and parks. Don't

be afraid to try something new! Goat yoga?... more

How Homeowners Can Save Money on Utility Bills | Better Mortgage

Here's a handy guide to help you save money on your utility bills.

Daily savings tips Did you know that making a few small tweaks

every day can significantly impact your energy usage and monthly

costs? Here are several new habits you can form and a few minor

adjustments you could make to save on your utility bills: The

temperature inside your home doesn't have to be exactly to your

liking while you're not there. You could save up to 10% on your

heating and cooling bill by adjusting your home's temperature by... more

New Homeowner Checklist: 5 Essential Things to Do When Moving In

Your real estate professional can assist with the right timing, or

perhaps your building manager if you're purchasing a new

construction home. If you're moving to a location that requires you

to switch providers, call the company or visit their website for

instructions on activating a new service. If you continue using the

same key handed over on your closing date, you're likely using the

same key used by the previous owner - and maybe even the owner

before them! Without swapping out locks, you may never know... more

Real Estate Attorneys: What You Need to Know | Better Mortgage

Better Attorney Match is currently available in New York, New

Jersey, Illinois and Massachusetts. The key difference is that an

attorney is a licensed legal professional while a real estate agent

is not. Your attorney is crucial to keeping your home purchase

running smoothly as broken communication can cause stress and

confusion. Many real estate professionals recommend choosing your

attorney right before you make your first offer on a home. In some

states, there is a review period that allows the buyer and... more

Cost cheat sheet for buyers, staging advice for sellers | Better Mortgage

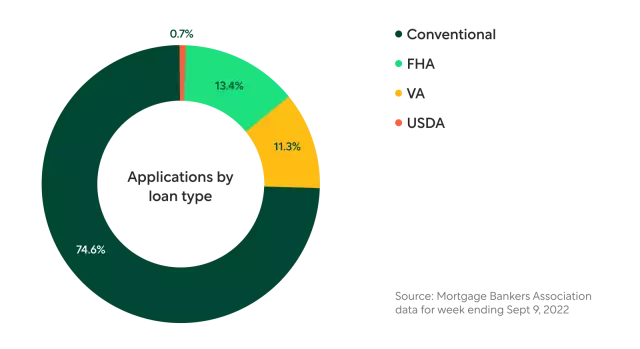

Down payments as low as 3.5% with an FHA loan First-time homebuyer

activity was up last week, and government loans made up a bigger

slice of the overall mortgage pie. With Better Real Estate, you

won’t pay commission to both your listing agent and the buyer’s

agent when your home sale closes. Local moving costs can on average

cost $1,682, according to HomeAdvisor. The buyer may cover many of

the closing costs. The seller may be responsible for some as well,

such as HOA fees or title insurance. For more information,... more

Loan forgiveness and listing agreements | Better Mortgage

Here's how: Debt is one of the key variables lenders use to

determine how safe or risky it would be to approve your loan. How

long should a listing agreement last? The moment you sign a listing

agreement with a real estate agent, the clock starts on your race

to the closing table. In a market where houses aren't moving as

fast as they once were, the expiration date of the listing

agreement is another important factor to consider: how much time

should you give an agent to sell your home before you move on?

Houses... more

Second Home vs Investment Property: What's the difference? | Better Mortgage

A second home must meet the following criteria to qualify for a

second home loan: The property must be suitable for year-round

occupancy, even if you only intend to use it part of the year. The

home may not be under the control of a property management company.

What is considered an investment property? An investment property

is also known as a rental property. Rather than occupying the home

yourself, an investment property should be leased to tenants to

generate rental income. Tax implications for a second... more

A Comprehensive Guide to a Second Home Loan | Better Mortgage

What is a second home loan? A second home loan is a mortgage used

to finance a secondary or vacation residence. For a property to be

considered a second home and deemed eligible for a second home

loan, it must meet the following guidelines: The home must be a

single-unit dwelling. Things to consider when financing a second

home While purchasing a second home is an exciting adventure,

financing requirements can be a bit more strict than those for a

primary mortgage. Second home loan mortgage requirements Here's... more

Contingencies, seller strats, and renos w ROI | Better Mortgage

Contingencies are the conditions both buyers and sellers must meet before a real estate transaction is finalized. In today’s correcting market, buyers don’t need to take such drastic measures to win bids on the homes they want. Instead of waiving contingencies, concentrate on finding homes in your budget and making offers that you’ll be able to afford. The renovations that have the highest ROI are restoring or refinishing hardwood floors. Get your custom rates in minutes with Better Mortgage.

Housing market corrections, buyer mindsets, and summer living | Better Mortgage

U.S. home prices are predicted to rise 0% next year, a dramatic shift from the 19.7% home price spike that occurred in the last 12 months. Sellers adapt slowly, but many sellers can’t resist pricing high in the hopes of cashing in on the tail end of the historic housing boom. Get in the buyer mindset to make your home appealing. Move-in ready properties are most appealing and stand out to motivated buyers. Work with an agent.

Buy-curious renters, staging tips, and water safety | Better Mortgage

Renting doesn't require repair and maintenance Owning a home comes

with day-to-day costs. Lifestyle factors outweigh some costs As a

renter you have less responsibility and more flexibility If you're

not ready to sacrifice that freedom, buying a home might not be the

right decision for you-even if the mortgage payment would be more

affordable than the cost of renting. If you're a buy-curious renter

but aren't 100% ready to commit to homeownership, consider the

benefits of rent-to-own agreements which give you... more

What a First-Time Homebuyer in Texas Should Know | Better Mortgage

The 2022 Texas Homebuyers and Sellers Report revealed that 32% of

all Texas homebuyers were first-timers. Benefits of buying a house

in Texas You know what they say: "Everything is bigger in Texas."

that includes the following benefits. Requirements needed to buy a

house in Texas Whether Texas is already your home or you're moving

from elsewhere for greener pastures, here's what you'll need to buy

a home in this state. Down payment for a house in Texas You'll

typically need to save for a down payment when buying... more

Real estate psychology + the power of equity in an uncertain economy | Better Mortgage

The two most important parties in any real estate transaction are

ultimately the ones who sit down on either side of that closing

table: the buyer and the seller. If you want to nab a home you can

afford in today's competitive market, consider thinking like a

seller. Most sellers are taking note and adjusting their

out-of-the-gate asking prices accordingly. With some sellers

feeling unsettling, price reductions are happening on a shorter

timeline than usual-in some cases, after just 14 days on the

market. You... more

Check out reforms, ask before you sell, and fireproof your property | Better Mortgage

Recent federal reforms could improve your homebuying options Buying

a home has traditionally been one of the most significant ways to

build wealth, but financing options have not always been equally

accessible. Today about 71% of white Americans own homes, compared

with 41% of Black Americans. If you struggled to qualify for

mortgage financing in the past, the reforms could improve your

chances: A new credit reporting system will allow rent payment

history to bolster creditworthiness-a factor that has

disproportionately... more

Leverage your lock, refresh outdoor spaces, and check local listing trends | Better Mortgage

One of the steps you'll take in the process of applying for a

mortgage or refinancing a current loan is "Locking" your interest

rate. While interest rates may fluctuate during the course of the

underwriting process, locking guarantees you a specific interest

rate for a set period-typically 30-60 days. Locking your rate helps

determine exactly how much your mortgage payment will be each

month. Until you lock, your interest rate are subject to daily

fluctuations based on how the mortgage market is doing. If you're... more

Hitting homebuyer stride, going low in listing limbo & beating buyer’s remorse | Better Mortgage

As more inventory floods the market, sellers who aren’t seeing competitive offers are likely to get antsy. Buyers who can outlast and outsmart the competition could be crossing the finish line having expended less money and effort. If they’re getting any bites in the first 10 days, a significant drop could generate buyer attention and help move the process along. You can likely afford to. The fact that housing prices have been on a steady upward trend.

Rising interest rates are causing some people to hit pause on their home search—and their hesitation is your opportunity. As competition cools and more listings go live, determined buyers are looking at a more level playing field for the first time in years. How should this shift in the market impact your shopping strategy?

Rising interest rates are causing some people to hit pause on their home search—and their hesitation is your opportunity. As competition cools and more listings go live, determined buyers are looking at a more level playing field for the first time in years. How should this shift in the market impact your shopping strategy?

Inventory waves, move-in readiness, and acing your maintenance phase | Better Mortgage

The inventory wave is cresting, but you still have to be in the right spot to catch it. Buyers in more competitive markets might have different expectations than buyers in less competitive areas. To get a sense of how move-in ready your home is, take a quick tour that covers the condition of the electrical, plumbing, and HVAC systems as well as the roof and major appliances. List your property with Better Real Estate. A Better Real Real Estate Agent can help you decide. Get your custom rates in minutes.

Adjustable-rate mortgages, inventory upswings, and summer listers | Better Mortgage

An adjustable-rate mortgage starts with a fixed interest rate for a set amount of time. That starting interest rate is typically lower than what’s available in fixed-rate mortgages. If you plan to relocate or upgrade to a bigger place in the next 5 years or so, you might want to consider an ARM. The math of supply and demand has driven up home prices, sparked an unprecedented frenzy of all-cash offers and escalated bidding wars. Buyers who buckle down and stay the course.

No Cash Out Refinance vs. Limited Cash Out Refinance: What You Need to Know Before Getting Started

There's no cash out, limited cash out, and even cash out

refinances. What is a no cash out refinance? A no cash out

refinance is often referred to as a "Rate-and-term" refinance.

Typically, no cash out refinances are a good option if you can

qualify for a better interest rate than when you first took out

your mortgage, perhaps due to a better credit score. As the name

suggests, a limited cash out refinance also allows you to take out

a limited amount of money, up to $2,000. Because a limited cash out

refinance... more

Buying or selling a home? Here’s what you need to know | Better Mortgage

See this week’s interest rates in action, get tips for fine-tuning any home buying budget, and find easy ways to improve the curb appeal of your home. Not available in all states. See better.com/about-us/licensing-disclosure.

Pros and Cons of a Cash Out Refinance | Better Mortgage

Learn the pros and cons of a cash out refinance to help you decide if the financial move is right for you. Not available in all states. See better.com/about-us/licensing-disclosure.

A Guide to a Cash Out Refinance | Better Mortgage

With a cash out refinance, you take out a new mortgage for more money than you owe on your current loan. The difference is paid to you in cash. Not available in all states. See better.com/about-us/licensing-disclosure.