Total Mortgage

How to Refinance an Inherited House - Total Mortgage

How to Use Gift Money for a Down Payment - Total Mortgage

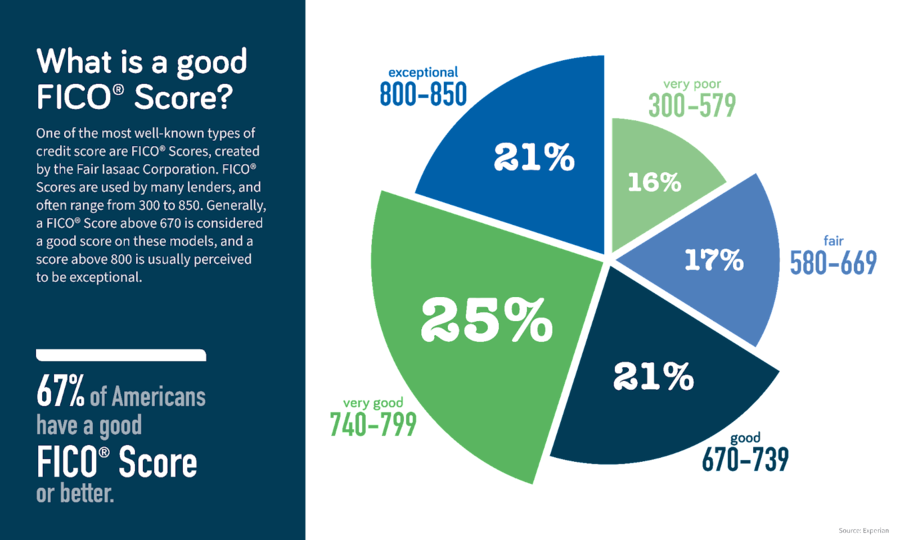

Credit Score & Home Buying: What Credit Score Is Needed to Buy a House? - Total Mortgage

When it comes time to purchase a house, a potential buyer’s credit score plays a critical role in the lender’s decision. If you are asking yourself, ‘what is the perfect credit score?’ the answer is that it depends.

Various factors are at play to determine the credit score needed to buy a house, and different mortgage products have their own unique credit score minimums attached.

In addition, each of the three credit bureaus — Experian, TransUnion, and Equifax — maintain their

... more

FHA vs. Conventional Loans: What’s Better For You? - Total Mortgage

How to Convince Your Landlord to Let You Renovate - Total Mortgage

USDA Home Loans: Everything You Need to Know - Total Mortgage

House vs Condo: What’s Better for a Second Home? - Total Mortgage

Understanding As-Is Sales: Risks and Benefits for Home Buyers - Total Mortgage

Can You Use Your 401k to Buy a House? Pros and Cons Explained - Total Mortgage

Getting a Home Loan Approval: How Long Does It Take? - Total Mortgage

As you’re starting the process of buying a home, you may be wondering how long everything takes. Specifically, you may be curious about how long the home loan approval process takes. Don’t worry, we’ve got you covered.

In this article, we’re going to highlight how long it takes to get approved for a home loan, as well as what you’ll need before starting the process.

The Home Loan Approval Process

The average time it takes to close on a home in the US is 51

... moreWhat Is Debt-to-Income Ratio and How Is It Calculated? - Total Mortgage

Your debt-to-income ratio, or DTI, signals your ability to repay a loan to your lender. A higher DTI means you carry too much debt compared to your monthly income, which could pose a greater risk to your lender.

By calculating your debt-to-income ratio, you can take the necessary steps to lower your DTI and get a better interest rate.

Here’s what you need to know about debt-to-income ratios, how to calculate DTI, and how it can impact your ability to qualify for a loan.

What

... more

Why Home Inspections Are Good For Buyers And Sellers - Total Mortgage

How to Refinance an Inherited Property to Buy Out Heirs [2023 Guide] - Total Mortgage

What is an Inspection Contingency Clause? - Total Mortgage

With today’s competitive market moving faster than ever, it can be easy to fall in love with a home too fast or cut corners in favor of a better offer. Our advice? Don’t. Before you close the deal, make sure everything is in check – and especially be aware of your home inspection contingency clause.

There are many variables and clauses included with your purchase agreement, but one of the most critical is the home inspection contingency clause. In this article, we’ll cover what inspection contingency

... moreGuide To Land Loans: What Are They & Types of Land Loans | Total Mortgage

How to Get a Mortgage When Relocating - Total Mortgage

How FHA 203K Loans Work and How to Qualify - Total Mortgage

For buyers working with a budget or current owners looking to upgrade their home, an FHA 203k loan comes with many benefits. Not only do FHA 203k loans wrap your renovation costs and mortgage into one payment, but it typically has easier income and credit requirements as well as a low down payment option.

Here’s what you need to know about FHA 203k loans and how to use this type of financing on your home improvement projects.

How Does an FHA 203K Loan Work?

An FHA 203k loan is a mortgage

... moreHome Loan Offset Account: What Is It and How Does It Work? - Total Mortgage

Boston Real Estate & Housing Market Prices | Total Mortgage

Boston is one of the hottest real estate and housing markets in the United States. However, even Boston experienced a slowdown in 2022 after the housing market faced several headwinds, making it more challenging for potential homebuyers to afford an increased down payment and mortgage.

As a result, price growth has been weak while homebuyers and sellers alike have often remained sidelined. According to CoreLogic’s deputy chief economist, Selma Hepp, home value growth rates in Boston declined to

... moreHow to Remove FHA Mortgage Insurance - Total Mortgage

How Are Interest Rates Determined and How Do They Work? - Total Mortgage

Interest rates are a critical factor in determining the cost of a mortgage and play a significant role in the housing market. They are determined by various factors, including monetary policy set by the Federal Reserve, demand for mortgage-backed securities on the bond market, and the creditworthiness of the borrower.

The Federal Reserve, through its monetary policy, sets the discount rate, which is the short-term interest rate at which banks can borrow money from the Federal Reserve. When the Fed raises

... moreHELOC on Rental Property: Home Equity Line of Credit Explained - Total Mortgage

If you are fortunate enough to own an investment property, you probably know something about generating additional income streams. You’ve heard about getting a home equity line of credit on your primary residence – but what about a rental?

If you are looking for more ways to access capital, you may be wondering if you can get a home equity line of credit, or HELOC, on a rental property. The answer is yes, though there may be some hoops you’ll need to jump through. If you’ve got adequate equity

... moreHome Inspection vs. Appraisal: The Big Differences to Know - Total Mortgage

The Complete Guide to Selling a House to a Family Member | Total Mortgage

They say not to mix family and money.

Sometimes, though, the stars line up perfectly and selling your house to a family member just makes the right kind of sense. Maybe it’s an old home that has sentimental value, or maybe you just want to give a leg up to a younger relative.

Regardless, having a buyer for your house already lined up keeps your home off Zillow and puts you in a great position.

1. Agree on a price, but stay flexible

In a standard real estate transaction, the

... moreCan You Get A Mortgage Without A Job? 6 Tips To Get Approved | Total Mortgage

There’s no arguing that having a job means you’re more likely to get approved for a mortgage. However, getting a mortgage without a job isn’t impossible, so if you’re gainfully unemployed and on the hunt for a house, check out these tips below.

1. Check the requirements

Every lender is different, so make sure you reach out and see what your lender’s specific requirements are.

Remember that lenders might have different requirements, but they all share one thing

... moreDoes Mortgage Pre-Approval Affect Credit Score? Here’s What You Need to Know - Total Mortgage

When you’re searching for your new home, a mortgage pre-approval will not only tell you what you can afford but can also help you stand out as a serious buyer. However, you’ll want to protect your credit score while you’re shopping for the best rate.

So, does a mortgage pre-approval affect credit score? Here’s how getting pre-approved impacts your credit score and how to shop for a mortgage without damaging your credit.

What Does It Mean to Get Pre-Approved for a Mortgage?

A

... more