You’re not alone. From the rise of tiny homes to the spiking interest in green housing ideas, people from all walks of life are rebelling against skyrocketing traditional home prices.

And it’s not just about money, either. With more Americans than ever working remotely, there’s less reason than ever to chain yourself to one location.

18 Alternative Housing Options

A decade ago, green homes were rare, as were tiny homes, accessory dwelling units, and smart home technologies that reduced energy usage.

Today they’re everywhere.

Whether you’re looking to save money, embrace a more eco-friendly or nomadic lifestyle, or just beat your own drum a little differently, scope out these ideas to get you excited about alternative housing.

1. House Hack with an ADU

Who wouldn’t want to live for free?

The idea is simple: you buy a home and find ways to have someone else pay the mortgage. The classic model is buying a small multifamily, and renting out the neighboring unit(s). Sharing walls with other housing units is inherently more eco-friendly than detached single-family homes, both in the use of building materials and energy efficiency. Here’s a detailed house hacking case study on how a 27-year-old with no real estate experience house hacked and currently lives for free in a beautiful suburban home.

If you don’t love the idea of living in a multi-unit building, or if multifamily properties are scarce where you want to live, you can house hack with an accessory dwelling unit (ADU). That could mean a basement or garage apartment, or a standalone structure like a carriage house or tiny home on your property. You can continue living in the main house if you like, or move into the ADU and rent out the main house. Not only would you collect more rent, but it will help you live more simply, and with a smaller environmental footprint.

Alternatively, you could rent out bedrooms to housemates in a single-family home. Deni and I have both done this, and it worked out beautifully.

In fact, Deni even house hacked her suburban single-family home by bringing in a foreign exchange student, and the placement service covered half her housing costs! A little creativity can go a long way, both with alternative housing and clever ways to cover your traditional house costs.

Compare mortgage terms on Credible, and keep in mind you can use the rents from neighboring units to help you qualify for the loan.

2. Tiny House in Tow

By now, everyone’s familiar with the tiny house movement. But tiny homes are good for more than just adding an ADU to your backyard. You can also use them to travel comfortably and even live nomadically, hitching up a tiny house to the back of your car or truck.

First, you don’t need a dedicated RV — you can keep your own car or truck, assuming it has enough power to pull a hitch. Which, let’s be honest, is usually much cheaper than buying an RV for your alternative housing.

Second, you don’t necessarily need to stay at RV parks for power and water. Many tiny homes have their own solar roofs, with rainwater reclamation and filtration systems for the ultimate green housing solution.

Beyond the warm-and-fuzzies of green housing, tiny homes with solar power and rainwater reclamation systems also help you stay self-sufficient. That means you can pull up just about anywhere you like, and settle in for as long as you like. Assuming the law doesn’t come shaking its stick at you.

Who needs a mortgage, anyway? Throw down $10,000-50,000 and go forth into the world!

3. RV Living

When you think of an RV, what do you picture? If you think of those rickety beige trailer-buses from the ‘70s, think again.

Today’s RVs often share more in common with luxury homes than trailers. Many include enormous “slides” — rooms that slide out of the main section to create a multi-room home when parked. From jacuzzi tubs, queen-sized beds, fully-equipped kitchens and comfortable bathrooms to any other amenity you could ask for, RV living is whatever you want it to be.

Or you could keep it simple with a classic camper van. Your choice.

Whether you earn $1,000/month or $10,000/month, consider a fun and mobile RV lifestyle at whatever luxury level you can afford. It sure beats overpaying for a dingy apartment!

My father-in-law doesn’t live full-time in his RV, but he and his wife take off for months at a time. They stay as long as they like at a given RV park, then move on. This is alternative housing at its finest.

On the other end of the spectrum, Paul and Nina live a frugal-but-fun and rewarding full-time life in their RV on a modest budget. They prove you don’t need much money for a fun nomadic life, and can take advantage of the many cheap unconventional housing alternatives out there. Your only limits are your own creativity.

4. Stay at a Campground

Many campgrounds offer RV parking, water, sewer, and electricity. In fact, I’m told that some campgrounds fill up for the year within minutes of opening reservations.

But you don’t have to have an RV to spend a month or two (or longer!) living at a campground. When I was younger, I used to stay at Cape Henlopen State Park’s campground, nestled between Lewes and Rehoboth Beach in Delaware. They had full bathrooms with showers, and fresh water pumps. My friends and I would spend all day on the beach, then shower and go out to restaurants and bars at night.

I never stayed longer than a week, but a determined camper could push those boundaries if they had a few solar chargers. As green housing ideas go, it doesn’t get much more eco-friendly than that.

Or much more affordable, for that matter.

5. Live on a Boat

Who says you have to live on land?

My sister Lauren dated a guy who wanted to live closer to her, so he bought a used houseboat for around $40,000 and rented a slip a few blocks down the waterfront Promenade in Baltimore’s Fells Point. It had two bedrooms, full electricity, a 46-inch LED television, heat, running water, and of course a motor.

I always thought they should have toodled down the coast, parking the house boat in the Florida Keys or somewhere equally enticing. They didn’t, alas. But I love how this other couple sold their home, bought a multifamily rental to become landlords, then bought a houseboat and are currently sailing around Europe. All with far lower living expenses than back home in the US.

If you’re interested, my fellow personal finance blogger My Money Wizard breaks down all the advantages to a houseboat, from cost to mobility to an upgrade in scenery and view.

Nor is a houseboat the only boat-based alternative to buying a house. Why not sail around the world with your spouse, significant other, or just a (really) good friend? Check out Kristin Hanes’s experience at The Wayward Home to see what it’s like to live full-time on a sailboat.

And ditch your assumptions about costs. Boats can offer extremely affordable housing with low energy costs, your own built-in outdoor space, and plenty of mobility.

Who needs a mortgage, anyway? Throw down $10,000-50,000 and go forth into the world!

(article continues below)

Free Masterclass: No Repairs or Renters — Earn 15-50% on Passive Real Estate Syndications

6. Prefab Cabins

Own some land? Pick up a prefab cabin!

Even better, build your own cabin using a cabin kit. My father and uncle did this — they bought a 10-acre lot near the Madison River in Montana, bought a three-bedroom log cabin kit, and spent a few summers building it.

It’s gorgeous, boasting solar panels for electricity, a rainwater reclamation system for running water, and a propane-powered on-the-fly hot water heater.

For heat, a pellet stove or wood-burning stove works wonders, and are cheap to buy and install.

Prefab cabins offer affordable, self-sufficient green housing options with low environmental impact.

7. Yurts

Yurts originated with the nomadic tribes of Central Asia, as round, dome-like tents. Today, people often use them for “glamping,” and they run the gamut from spare and easy to move to luxurious and semi-permanent.

You can buy comfortable, high-end yurt kits online for between $5,000 – $10,000, with the glaring addendum that “some assembly is required.” Note that yurts tend not to have electrical wiring or plumbing, so people typically use composting toilets with them.

Consider erecting a yurt on your property to rent on Airbnb for vacationers looking for a unique glamping experience. You could also build a yurt on land that you own, whether to rent to campers or to use yourself.

Or, if you’re feeling adventurous, you could try moving around with a yurt that’s easy to set up and collapse.

8. Housesit

Not everyone without a permanent address is homeless. Why not go live in other people’s homes?

Want to stay for free in others’ homes? Offer to housesit! For free matchmaking services for pet owners and house sitters, check out TrustedHousesitters.com, Rover.com, or HouseSittersAmerica.com. In most cases, you do have to care for other people’s pets while they’re away. But that’s a small price to pay for free rent at upscale homes.

Additional options include Craigslist, local pet owners’ groups on Facebook, and local Realtors.

While some people use housesitting to score free accommodations while traveling, others actually live as full-time nomads housesitting for other people. Check out Brittnay and Jayden’s blog about housesitting full-time for a fun example.

9. Home Swaps

When you travel, your house sits vacant and unused.

But just as you need a place to stay when you visit another city, other vacationers need a place to stay when they visit your city. Housing swap websites offer a network of people who make their homes available while they aren’t using them, so you can stay at other people’s vacant homes and they can stay at yours.

In the classic housing swap, you and someone else literally swap homes for a week or however long you like. But that’s hard to arrange, finding someone in the exact place you want to go who also wants to visit your city — on the exact same dates.

So websites like HomeExchange.com let you accrue Guest Points as a house swap currency. When people stay at your home, they pay you in Guest Points. When you stay in other people’s homes, you pay them with Guest Points.

Think of it like Airbnb, but instead of paying with money, you barter home stays.

For nomads looking to spend much of the year traveling, you can theoretically stay for free indefinitely at unique homes around the world, for endless alternative housing options.

10. Airbnb & Geoarbitrage

If you hadn’t noticed, the cost of real estate isn’t exactly the same everywhere.

The cost per square foot of housing space in San Francisco is around $1,100(!). In Buenos Aires, the cost per square foot is around $167.

You can live like a king on a modest income in some parts of the world, or live like a pauper on a high income in others. So stop thinking so linearly about where you live, and start exploring parts of the world you never considered before. Research places with a high quality of life at a low cost of living.

Having traveled all over this planet, a few that come to mind for me include:

Buenos Aires, Argentina

Prague, Czech Republic

Montevideo, Uruguay

Cape Town, South Africa

Abu Dhabi, UAE

Plovdiv, Bulgaria

Budapest, Hungary

Go stay for a month at an Airbnb or VRBO vacation rental. If you like it, consider moving there permanently.

11. Teach Abroad & Live for Free

My wife Katie is a school counselor, who spent the first four years of her career in Maryland. Then she took a job at an American school in Abu Dhabi, where we thought we would spend two years as a fun adventure before moving back to the US.

That was eight years ago. We still live abroad, currently in Brazil.

International educators get not just a comparable (or higher) salary than in the US, but they often get free furnished upscale housing, full comprehensive health insurance, and paid flights home to the US each year.

Couple that with the fact schools typically put you up near campus, so you may not need a car. Katie and I shared one car for the four years we lived in Abu Dhabi, and didn’t bother getting a car at all in Brazil.

That means that three of the largest expenses for most households — housing, transportation, and health insurance — are completely removed from our budget. We can save and invest all of the money we would otherwise have spent on them.

Here’s the island where we lived for free in Abu Dhabi:

12. Shipping Container Homes

Once considered a novelty, shipping container homes have come a long way.

Think of shipping containers as lego building blocks, that architects and home designers can mix and match any way they like. You can create a home that shows off its roots, or a home that you can’t tell was constructed from old shipping containers.

Not only are these homes more affordable to construct, but they’re also incredibly durable. And that says nothing of the environmental impact of recycling old shipping containers to build sturdy, beautiful homes rather than cutting down trees to do it.

(article continues below)

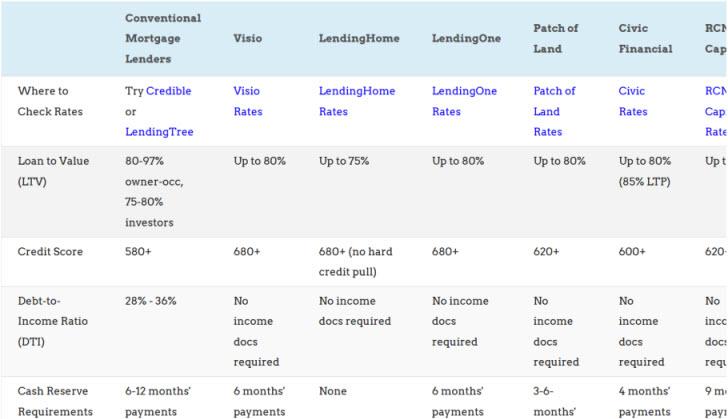

Want to compare investment property loans?

What do lenders charge for a rental property mortgage? What credit scores and down payments do they require?

What do lenders charge for a rental property mortgage? What credit scores and down payments do they require?

How about fix-and-flip loans?

We compare the best purchase-rehab lenders and long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

13. Boxcar Homes

The same principle applies with boxcar homes. But instead of using old shipping containers, builders recycle old train cars.

On the downside, boxcars don’t combine easily like shipping containers. That limits your options for building larger or complex homes.

But as a tiny house, boxcars offer plenty of character, with minimal cost to convert. And like shipping container homes, they reuse existing structures to create a new home, rather than having to use new materials.

Since they once served as a mode of transportation, many boxcar homes lend themselves to towing behind a truck as well.

Here’s an example of what they can look like as homes:

(image courtesy of Goods Home Design)

14. Pallet Homes

Many people and companies consider wooden pallets to be commercial waste. They literally just throw them away.

But it’s useful wood, already constructed into building blocks. That means you can get the framing for free, to construct a modest DIY house out of recycled materials.

Again, it offers an eco-friendly alternative source of building materials, using existing wood for framing. Just beware that these homes may not be sturdy enough to withstand extreme weather, if you live along the path of frequent hurricanes, tornadoes, or earthquakes.

(image courtesy of 99 Pallets)

15. Silo Homes

What happens to the silos when a farm closes down?

In a perfect world, they become the structure for a home.

Or part of a home, if you prefer. You can incorporate a silo as simply one architectural element in a more traditional home, to give it some unique personality and flair.

You can often pick up old silos for free, or rather for the cost of hauling them away. And once more, you get to reuse existing building materials.

If you like the idea of rustic charm for a do-it-yourself homebuilding project, look into converting a silo into a home.

(image courtesy of Decoist)

16. Earth Berms/Hobbit Holes

We all fell in love with Bilbo Baggins’ hobbit hole in The Lord of the Rings. But I didn’t realize people actually built and lived in these until I saw a Welsh guy and his father-in-law build one in the late 2000s.

They dug and built the hobbit hole house in four months with no heavy construction equipment, and created a gorgeous, infinitely livable home. And they used nothing but locally available building materials, such as stone from the dig-out, tree branches, and lime plaster. Straw bales provided breathable flooring and wall insulation, and of course all hobbit holes have a green roof.

See the details of how they built this eco-friendly hobbit hole here.

You can also buy prefabricated shells to embed in hillsides as earth shelter homes. That spares you having to frame out the walls and roof, and offers more moisture protection, but comes with higher costs. Learn more at providers like Green Magic Homes.

As green housing ideas go, hobbit holes offer built-in insulation for energy efficiency. They stay cool in the summer, and if you get chilly in the winter, a fireplace, wood-burning stove, or pellet stove can heat the entire house.

17. Cob Houses

As an alternative to modern building materials, you can go old school with cob houses.

Cob or cobb is a type of earth masonry, made with subsoil such as clay, fibrous organic material, and sometimes lime. Made properly, it’s as strong as concrete, but more attractive, temperature regulating, and environmentally friendly.

You can build charming cottages that look like they stepped out of a fairy tale with cob. Check out a few examples to see what I mean:

Image: Thannal

Image: Michael Buck

18. Treehouses

What kid doesn’t want to live in a treehouse?

If your inner child never quite let go of that dream, consider building a habitable treehouse. Treehouses come with some challenges, since you’re building the structure around a living organism that constantly grows, moves, and changes.

But you win infinite style points for a proper treehouse.

As a variation on treehouses, you can also install a free spirit sphere in a large tree. It hangs suspended — securely — from the tree.

Final Thoughts

As someone who hasn’t paid full price for housing since 2011, I’m all about alternative housing ideas.

That could mean more travel-oriented housing alternatives such as RVs, houseboats, housesitting, or housing swaps. Other people get more excited about green housing ideas such as earth berms, cob houses, silo homes, shipping container homes. And some combine travel with green housing options like tiny homes that you can take anywhere.

Many of these green housing alternatives are also self-sufficient. Eco-friendly homes often include rainwater reclamation systems for water, small Energy Star appliances, and solar panels or green roofs.

Bear in mind that many parts of the world use housing with a far lower energy consumption than the US. My apartment in Brazil uses an electric tankless water heater for the showerhead, and requires no central heating or air conditioning because the climate is mild year-round. Our home has almost no carbon footprint.

Think outside the box when you explore sustainable homes. You can find cheap alternative housing ideas in other countries that offer green home designs at a fraction of the cost of similar homes in the US.

What alternatives to buying a house have you considered (or done)? Share your experiences and thoughts on alternative housing in the comments below, we love hearing from readers, and are always looking for case studies to feature!

More Unconventional Reads:

How to Invest $1,000 in Real Estate

How to Find Good Deals on Investment Properties – Even in a Hot Market

About the Author

G. Brian Davis is a landlord, real estate investor, and co-founder of SparkRental. His mission: to help 5,000 people reach financial independence by replacing their 9-5 jobs with rental income. If you want to be one of them, join Brian, Deni, and guest Scott Hoefler for a free masterclass on how Scott ditched his day job in under five years.

I want to know more about…

Connect with us on social!

less