1 Follower

713 Views

nationalmortgageprofessional

1 Follower

713 Views

128

Posts

Planet Home Joins Other Lenders Offering Buydowns

Now offers 2-1 and 1-0 seller-paid buydowns on its core loan products.

Class Valuation Acquires PropertyVal

Appraisal management company expands its presence in N.H., Maine.

New York Appeals Court Sides With Fannie Mae

Decision in a foreclosure case could have an impact on legislation pending in the Empire State.

Academy Mortgage Settles Underwriting Fraud Lawsuit For $38.5M

Utah-based company accused of improperly originating and underwriting mortgages insured by FHA.

ATTOM: Home Flipping Declined During 3Q

The third quarter saw 92,422 single-family houses and condominiums in the United States flipped.

The Fed Hikes Interest Rate 0.5%, Raises Target For '23

The 50-basis-point hike is 7th in 2022, but target range for 2023 is still 85 basis points higher.

New York Mortgage Trust Appoints New President

Managing Director Nicholas Mah takes over the post effective Jan. 1.

MISMO Names Acting President As Appleton Departs

VP of Operations Jan Davis to serve as interim president until a permanent replacement is chosen.

Wells Fargo 3Q Earnings Take A $2B Hit

Hurt by operating losses due to legal & regulatory issues, and by falling mortgage originations.

Equifax To Offer Expanded Bill Payment History To Lenders

The program is designed to expand the pool of potential homebuyers.

Federal Agencies Announce Threshold for Smaller Loan Exemption

The 2023 threshold will involve exempting loans from special appraisal requirements for higher-priced mortgage loans.

Redfin: Housing Activity Plunges As Rates Reach 20-Year High

Price drops also reached a new high as home sales & listings start to decline.

JPMorgan Chase 3Q Profits Down 17% YOY

While net income also fell from previous quarter, results still beat analysts expectations.

Fitch Rates Non-QM Offering By PRPM 2022-NQM1 Trust

The loans were originated by Sprout Mortgage, Newfi Lending, and others.

Bank Associations Sue The CFPB Over Discrimination Regulations

The lawsuit claims the CFPB is exceeding its statutory authority outlined in the Dodd-Frank Act.

Remembering Steven Schnall, Quontic Bank CEO

Industry News Remembering Steven Schnall, Quontic Bank CEO Katie

Jensen Aug 04, 2022 Schnall died in a motorcycle accident while on

his way back from a biking trip to Canada. Quontic Bank CEO Steven

Schnall, who built a thriving mortgage business focused on New

York's immigrant communities and moonlighted as a boutique condo

developer, passed away this week. Sources confirmed with The Real

Deal that Schnall died in a motorcycle accident while on his way

back from a biking trip to Canada. On a podcast last year,... more

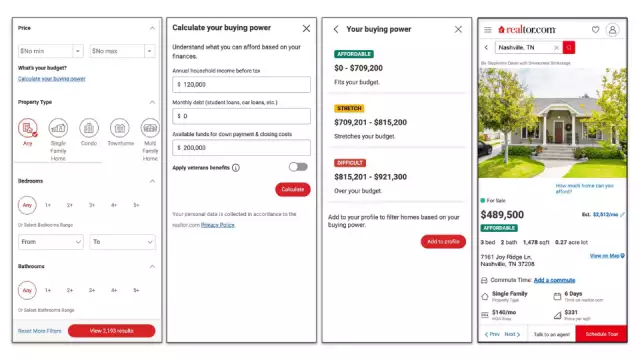

Realtor.com Releases Home Affordability Tool For Consumers

Industry News Realtor.com Releases Home Affordability Tool For

Consumers Katie Jensen Aug 04, 2022 More than two-thirds of

shoppers were surprised by what they could actually afford for

their first home. Realtor.com has introduced a new buying power

tool to help home shoppers see whether a specific home is

"Affordable," "a stretch," or "Out of reach." To give buyers a more

objective view of their budget, the tool uses a home shopper's

specific financial details, current mortgage rates, taxes,

insurance, and... more

Home Prices Outpace Inflation

A new single-family home has a median square footage of 2,356 and a price of $397,100. In 1980, the median price per square foot of a U.S. home was only $41, 310% less than today’s price. Memphis has the smallest square footage overall, at just 1,376 sf. Miami has the largest square footage. Suburban and rural areas are best for buyers looking for more space. The average number of people per household has slightly decreased from 2.8 to 2. 5.5.

Black Knight 2Q Earnings Fall 88% From 1Q

Second quarter of 2022 was a busy one for Black Knight, which saw a dramatic decrease in quarterly earnings. Revenues totaled $394.5 million in the second quarter, up 1.9% from the first quarter of last year. The results were below the consensus of analysts surveyed by Zacks Investment Research, which had predicted quarterly earnings of 60 cents per diluted share.

For 1st Time Since April, Mortgage Rates Dip Below 5%

Freddie Mac says mortgage rates slid to 4.99% this week, the first

time since April they've been below 5%. Freddie Mac on Thursday

released its weekly Primary Mortgage Market Survey report. The last

time mortgage rates were in the fours was the week of April 7, when

they stood at 4.72%. The survey is focused on conventional,

conforming, fully amortizing home purchase loans for borrowers. A

year ago at this time, the 15-year FRM averaged 2.40%. The 5-year

ARM averaged 4.50% and 4.20%. The 15- year FRM averaged... more

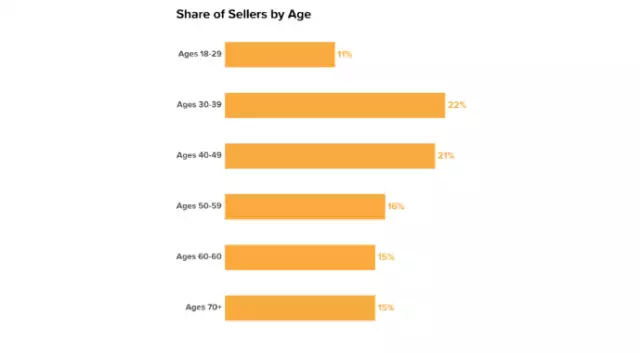

Zillow Offers Look At Typical Home Seller

Of the dual seler-buyers, 4% upgraded to buying a more expensive

home than the one they sold, a sharp drop from 2021's 55%. Sellers

who included a virtual tour in their home listing were more likely

to report receiving at least 1 all-cash offer vs. sellers without a

virtual tour. The typical U.S. home seller is white, 46 years old,

has household income in the low $80,000 range, and is also buying a

home. The report's data broadly showed that most sellers are

partnered, married, or previously married, have at... more

nCino Announces Executive Leadership Appointments

Matt Hansen has been named chief product officer of nCino, overseeing the company’s product development & engineering organization globally. Jaime Punishill will take on a new strategic role with the company after serving as CMO since 2012. Ben Miller is named CEO of SimpleNexus, an ncino Company, succeeding Cathleen Schreiner Gates. In his new role, Miller will oversee the continued growth and expansion of the SimpleNExus business and drive innovation that continues to drive innovation.

Class Valuation Acquires AppraisalTek

Class Valuation acquired AppraisalTek (ATek), a nationwide appraisal management company with a large footprint in the Western region of the United States. Financial terms of the transaction were not disclosed. Atek’s staff appraiser network and strong reputation for solid relationships, superior customer service, and robust performance will bring meaningful value to its customers. ATek operates in all 50 states and the D.C.

KBRA Assigns Preliminary Ratings To Non-QM Offering VERUS 2022-7

Non-QM Investor Loans

... more

... more

KBRA Assigns Preliminary Ratings To Non-QM Offering VERUS 2022-7

David Krechevsky Jul 26, 2022... more

Sink Or Swim: Which Areas Are Destined To Survive The Recession?

Analysis and Data

Sink Or Swim: Which Areas Are Destined To Survive The Recession?

Katie Jensen Jul 26, 2022

The outcome won’t be the same across the nation — some areas

... more

Nations Lending Continues Midwest Growth With New Illinois Branch

Career Industry News

... more

... more

Nations Lending Continues Midwest Growth With New Illinois Branch

Keith Griffin Jul 26, 2022... more

New-Home Sales Fell Sharply In June

Analysis and Data New-Home Sales Fell Sharply In June David

Krechevsky Jul 26, 2022 Sales of new single-family homes fell 8.1%

in June from May. KEY TAKEAWAYS Sales of new homes posted a

seasonally adjusted annual of 590,000 nationwide in June, down 8.1%

from May and down 17.4% from June 2021, according to the U.S.

Census Bureau. The supply of new homes for sale at the end of June

was up for the fifth consecutive month. The nationwide decline in

sales in June reversed the surprising increase in sales reported... more

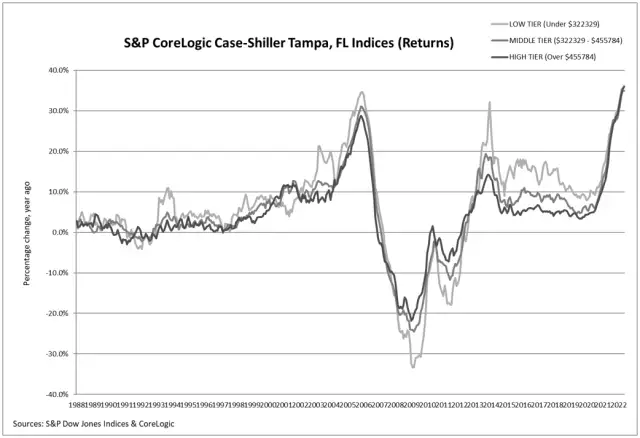

S&P CoreLogic Reports A 19.7% Annual Gain For May

KEY TAKEAWAYS The 10-City Composite annual increase came in at 19%,

down from 19.6% in April. U.S. National Index posted a 1.5%

month-over-month increase in May. The S&P CoreLogic

Case-Shiller U.S. National Home Price NSA Index, which covers all

nine U.S. census divisions, reported a 19.7% annual gain in May,

down from 20.6% in the previous month. The 10-City Composite annual

increase came in at 19%, down from 19.6% in the previous month.

Tampa, Miami, and Dallas reported the highest year-over-year gains

among... more

Ribbon Expands into Kentucky; Now In 15 States

Industry News Tech

Ribbon Expands into Kentucky; Now In 15 States

David Krechevsky Jul 26, 2022Cash-offer fintech expands

... more