Mortgage News Daily

Quiet Conclusion to a Raucous Week

No Help From Data Today

Data Calling Fed's Confidence Into Question

2 Out of 3 Reports Agree Rates Should be Higher Today

Calmer Day of Losses. Data Resumes on Thursday

Quiet, Data-Free Session Leaves Focus on Treasury Auction

Volatility After CPI, But Only Moderate Weakness

Paradoxical Initial Reaction to Hotter CPI, But The Day is Young

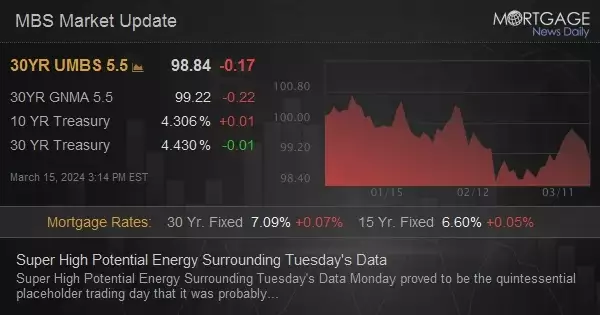

Super High Potential Energy Surrounding Tuesday's Data

Time to Find Out if The Last CPI Report Was an Outlier or Warning Shot

Resilience Threatened by Data at Home and Abroad

More Signs of Resilience Amid Month-End Buying Spree

More Signs of Resilience Amid Month-End Buying Spree

It was a generally resilient day for the bond market after a bit of a scare in the morning. European inflation data caused a sell-off in EU bonds that spilled over to Treasuries overnight. Selling continued in the first few hours, but bonds began to recover after a slightly weaker Chicago PMI report. A calm, sideways mid-day gave way to stronger buying as month-end trades crowded in before the 3pm CME closing bell. Month-end buying aside,

... more

US Bonds Fighting Against European Weakness

The message from today's overnight trading session is clear: European yields have broken well above their most recent ceiling after hotter inflation data in Spain and France. That ceiling had seen similar activity to the US version at 3.98% in 10yr yields. Today begins with US bonds fighting to stay inside the sort of range that EU yields just abandoned.

In other news,

... more

Bonds Hold Ground Despite Onslaught of Corporate Issuance

Sell-Off Finally Showing Signs of Fatigue

Weaker After PCE Data, But it Could Have Been Worse

Weaker After PCE Data, But it Could Have Been Worse

PCE Inflation data has been relegated to an "occasional and modest" market mover in the current environment. Traders have been doing whatever they need to do in response to the comparable CPI data that comes out much earlier in any given month. But exceptions are made for PCE data that sings a decidedly different tune, such as today's. It matched a decades-high reading at the core level (month-over-month) and thus sent yields higher. Despite

... more

There's Still a Chance, But...

Ceiling Signs or Is It a Trap?

Mixed Start as Bonds Feel Out New Range

At some point during the current selling spree, bonds will find a point of equilibrium where traders feel they've adequately protected themselves from the prospect of sticky inflation and economic resilience. They clearly didn't feel protected with 10yr yields under 3.5% several weeks ago. While we started the week with more selling, the past 2 days have been more balanced (and largely trading inside Tuesday's range). Patterns like this can simply be consolidations before more selling, but they can

... more

This Is How They Get Ya!

Do Today's Fed Minutes Matter?

Data Fuels Ongoing Scramble Toward Higher Rates

Data Fuels Ongoing Scramble Toward Higher Rates

Almost the entire month of February has been a mad dash from the lowest rates in months to the highest rates in months. The whole ordeal can be traced back to several key economic reports with mid-tier reports occasionally piling on. Today saw a surprisingly large reaction to mid-tier data (S&P/Markit PMI). The only way to reconcile the disproportionate reaction would be to add some extra overseas selling from the holiday closure and the overnight

... more

February Has Quickly Changed The Rate Outlook

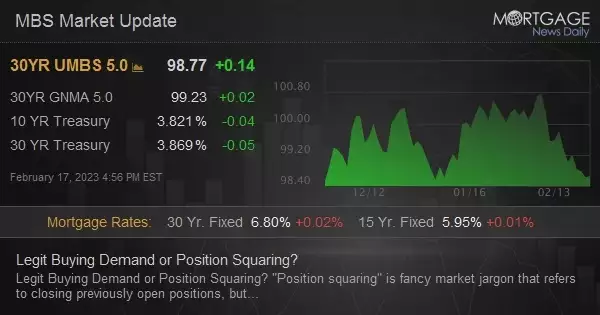

Legit Buying Demand or Position Squaring?

Legit Buying Demand or Position Squaring?

"Position squaring" is fancy market jargon that refers to closing previously open positions, but it can also refer to taking opposing positions to square up one's risk exposure. A "position" is just a bet on rates moving higher or lower. Traders have been in short positions on rates this week (i.e. betting on rates going higher). Is the squaring of these positions for the 3-day weekend the only way to explain today's moderate mid-day improvement or

... more

Limited Data and Events; Limited Inspiration For Rallies

The current landscape is fairly simple. The bond market has been in the midst of a "repricing" event following the jobs report at the beginning of the month. Traders are "repricing" expectations for the Fed rate hike outlook. This has spilled over into longer-term rates. Until we have clear momentum heading in a friendly direction, the path of least resistance is for rates to continue redefining a new, higher range after failing to break through the new, lower range that was seen in December and January.

... more

Another Day, Another Sell-Off

Another Day, Another Sell-Off

Bonds may not have sold off in an overly excessive manner today, but they sold off nonetheless. In other words, rates went higher. The early culprits were twofold: a surprisingly hot Producer Price Index and some comments from Fed's Mester on the prospect of a 50bp rate hike. Then in the afternoon, Fed's Bullard said similar stuff and went a step further, saying he wouldn't rule anything out for the next meeting. All this after Fed members spent the past 3 weeks

... more

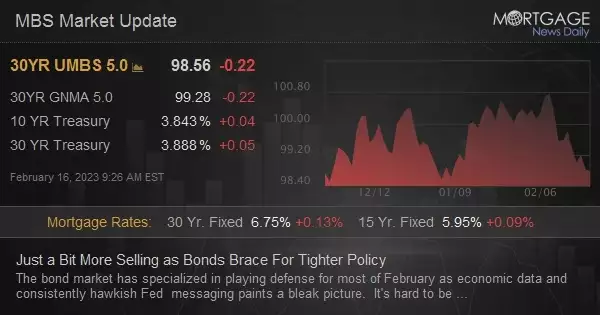

Just a Bit More Selling as Bonds Brace For Tighter Policy

More Yield Curve Musings and Retail Sales Reaction

Retail Sales Data Not Doing Rates Any Favors

More Data to Prove The Fed's Point; Rates Don't Like It

More Data to Prove The Fed's Point; Rates Don't Like It

It will take one of two things for the current rising rate trend to run its course. Either the economic data needs to shift in a compelling way or the selling needs to take rates back up to 2022's highest rates at which point markets will conclude a compelling economic shift is imminent. Neither option is "fun" for the mortgage/housing market. Today's CPI wasn't as much of a barn burner as the jobs report 2 weeks ago, but it was high enough

... more