Navigating the NYC Co-op Market: A Comprehensive Guide

Navigating the NYC Co-op Market: A Comprehensive Guide

Introduction: Understanding the Appeal of NYC Co-ops

New York City's housing market offers a unique proposition unlike anywhere else in the United States: cooperative apartments, known as co-ops. This guide dives deep into the complexities and charms of buying a co-op in NYC, providing potential buyers with essential insights into why these properties are both coveted and challenging.

What Is a Co-op Apartment?

Defining NYC Co-op Ownership

In the heart of the bustling city, co-op apartments offer a distinctive form of housing. Unlike traditional home purchases, buying a co-op means acquiring shares in the corporation that owns the building. These shares entitle you to occupy a specific unit, effectively making you a shareholder rather than an outright owner of the property. This communal approach is deeply integrated into NYC’s urban fabric, making co-ops a popular choice among city dwellers who value community living and a shared sense of ownership.

Co-ops typically have a board of directors elected by shareholders who oversee the building's management and enforce rules. This governance structure ensures that all residents adhere to community standards, fostering a stable and cooperative environment. It also means that every potential buyer must be approved by the board, which involves a thorough vetting process.

Financial Aspects of Co-op Ownership

Cost Advantages of Co-op Apartments

One of the primary attractions of co-op apartments is their relative affordability compared to condominiums. This affordability extends beyond the purchase price, as co-op transactions often come with lower closing costs. Unlike condo sales, co-op purchases typically do not incur mortgage recording taxes or require title insurance. These savings can make a significant difference, especially in a high-cost market like NYC.

However, prospective buyers should be aware that co-ops also come with substantial financial barriers to entry. Co-op boards usually require significant down payments—often as much as 20-50% of the purchase price—and impose strict debt-to-income ratio requirements. These measures help maintain the financial stability of the co-op community, ensuring that all residents are financially sound and capable of meeting their obligations.

Moreover, monthly maintenance fees for co-ops can include property taxes, utilities, and building maintenance costs, which are typically higher than those for condominiums. Understanding these financial obligations is crucial for buyers to accurately assess the affordability of a co-op.

The Co-op Board Approval Process

Navigating the Entry Barriers

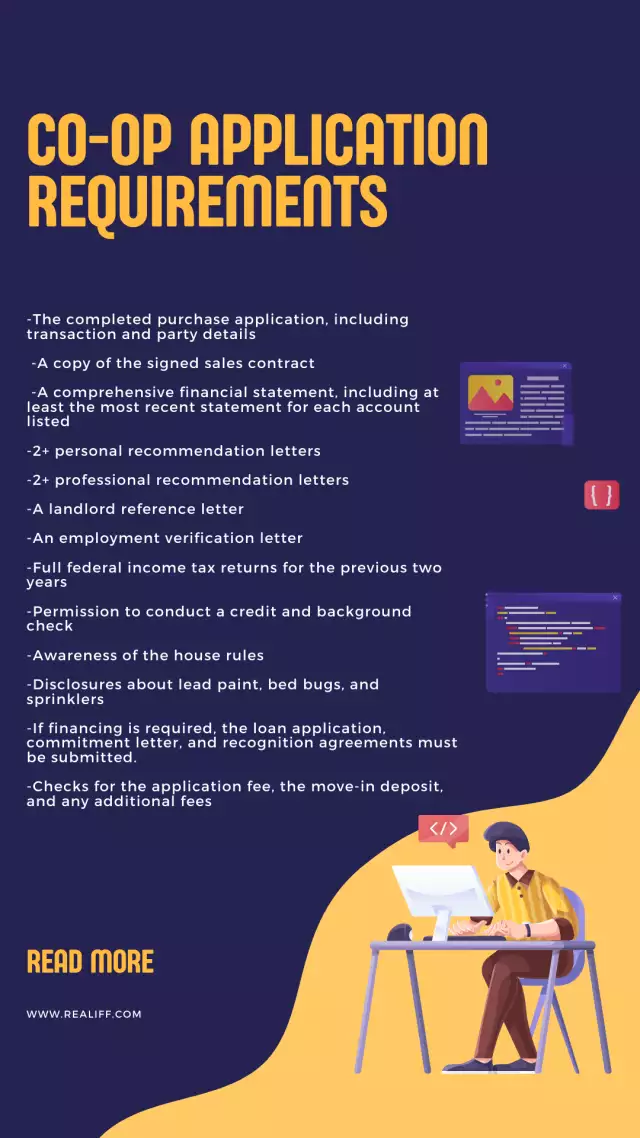

Buying a co-op in NYC involves more than just securing a mortgage and making an offer. Prospective buyers must pass through a rigorous approval process conducted by the co-op board. This process includes a comprehensive financial review, background checks, and often a personal interview. The goal is to ensure that new members are financially stable and will contribute positively to the community.

The financial scrutiny involves submitting detailed documentation, including tax returns, bank statements, and proof of income. Buyers must demonstrate a strong financial position and often maintain significant reserves post-purchase. The personal interview assesses the buyer's compatibility with the community and their willingness to adhere to the building's rules.

While this process can be daunting and invasive, it serves an important purpose. It helps protect the community from potential financial or behavioral issues, contributing to the overall stability and cohesiveness of the co-op.

Living in a NYC Co-op: Community and Regulations

The Social Dynamics of Co-op Life

Living in a co-op in NYC offers a unique community experience. Residents often engage more directly in building management and decision-making processes, creating a collaborative and involved atmosphere. This sense of community can be a significant draw for many, fostering relationships and a collective sense of ownership.

However, co-op living comes with strict regulations that govern various aspects of daily life. These can include rules on subletting, renovations, and the resale of units. For instance, many co-ops have policies that restrict or outright prohibit subletting, aiming to maintain a stable resident population. Renovation projects often require board approval, ensuring that changes align with the building's standards and do not disrupt other residents.

Additionally, co-ops may impose flip taxes—a fee paid to the co-op upon the resale of the unit—which can affect the net proceeds from a sale. These regulations are designed to preserve the community's character and financial health but can limit personal flexibility.

Evaluating the Pros and Cons of Co-op Living

Co-op living in NYC has its distinct set of advantages and challenges.

Pros:

- Affordability: Generally lower purchase prices and reduced closing costs compared to condos.

- Community Engagement: Stronger sense of community and collective decision-making.

- Stability: Rigorous approval process helps maintain a financially and socially stable environment.

- Inclusive Maintenance: Monthly fees often cover more services, including property taxes and utilities.

Cons:

- Invasive Approval Process: Extensive financial scrutiny and personal interviews can be daunting.

- Limited Flexibility: Strict rules on subletting and renovations can restrict personal freedom.

- Potential Lack of Modern Amenities: Some co-op buildings might lack the modern conveniences found in newer condos.

- Higher Monthly Fees: Maintenance fees can be higher and may include shared costs for building-wide expenses.

Is a Co-op the Right Choice for You?

Making an Informed Decision Based on Personal Goals

Deciding to buy a co-op in NYC involves a careful evaluation of your personal preferences, financial readiness, and long-term housing goals.

For those who appreciate the benefits of community engagement and can meet the stringent financial requirements, co-op living can be highly rewarding. The sense of belonging and involvement in building decisions can enhance your living experience.

However, if you prioritize autonomy over your property and prefer less invasive financial scrutiny, the constraints of co-op living might feel too restrictive. Evaluating these factors in the context of your lifestyle and financial situation will help determine if a co-op is the right choice for you.

Conclusion: Your Pathway to Buying a Co-op in NYC

Buying a co-op in NYC offers a blend of affordability and community engagement set against the vibrant backdrop of one of the world's most dynamic cities. While the process can be complex and challenging, platforms like Realiff.com provide invaluable resources, expert advice, and comprehensive tools to help you navigate the NYC real estate market. Realiff.com stands out as a premier resource, empowering buyers to make informed decisions and find the perfect co-op that aligns with their goals.

Essential Questions About Buying a Co-op in NYC

Why choose a co-op over a condo?Co-ops often offer lower prices and a stronger community feel, which can be appealing for those looking for a sense of belonging.

When is the best time to buy a co-op?Timing should align with your personal financial stability and favorable market conditions. It's essential to be prepared for the rigorous approval process at any time.

Where are the best co-ops located in NYC?Research neighborhoods to find a community that matches your lifestyle and budget. Areas with established co-op buildings often provide more stable investment opportunities.

What are the biggest challenges in buying a co-op?The approval process and financial scrutiny can be significant hurdles. Understanding these challenges and preparing adequately can help navigate them successfully.

Who can help you navigate the purchase of a co-op?Utilize experienced real estate agents, particularly those with a strong track record in co-ops. Their expertise can be crucial in managing the complex approval process.

How do you prepare for buying a co-op?Get your financial documents in order and be ready for a thorough approval process. Engaging with knowledgeable professionals early can streamline your journey.

Realiff.com offers tools, advice, and real-time listings to help you explore co-op options in NYC, ensuring that you are well-prepared to take this significant step in your real estate journey.