Home sellers are cutting list prices as more buyers take pause: 'The market is not the same'

Home sellers are cutting list prices as more buyers take pause: 'The market is not the same'

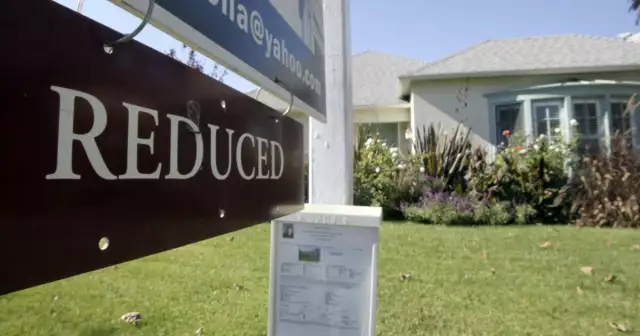

Home sellers are increasingly cutting their asking prices as buyers, constrained by higher mortgage rates and overall inflation, have become less willing to jump into the housing market at any cost.

The growing number of price cuts, a trend showing up in data from Southern California and across the nation, is one of the strongest signs yet that the previously red-hot market, fueled by low mortgage rates and all-cash bidding wars, is cooling.

The price reductions don’t mean overall home values are dropping. In Southern California and the wider U.S., they make up a minority of listings, and most homes still sell for more than the list price.

Industry experts, for now, do not see a plunge coming in the housing market, catapulted to record-high prices in the first two years of the pandemic as many people sought out more space and had new savings to spend.

Values could come down modestly, some experts said, if the Federal Reserve’s actions to tame inflation send mortgage interest rates significantly higher — or tip the economy into recession.

For buyers, the market already feels significantly different from the frenzied competition of several months ago.

“The market is not the same as it was a month ago even,” said Lindsay Katz, a Los Angeles agent at Redfin, the brokerage company.

On Covello Street in Van Nuys, the owner of a four-bedroom house recently cut the price by $50,000 to $949,900 after the 1950s tract home sat on the market for three weeks.

Other homes in the area are listing even bigger price reductions: a $78,000 cut for a two-bedroom home, and a house with an accessory dwelling unit first listed at $1 million now for sale at $860,000 — a $140,000 price cut.

Katz doesn’t represent the Van Nuys listings, but similarly had to recently cut the price on a Woodland Hills four-bedroom home by $40,000.

The explanation for the dramatic shift is simple, according to real estate experts. Mortgage interest rates have shot up in recent months, quickly making housing much more expensive.

Monthly mortgage payments for a same-priced home are now hundreds of dollars — sometimes upward of $1,000 — more than what they were at the beginning of the year, when rates were in the 3% range.

The change has placed some buyers in entirely new price brackets and priced others out altogether.

“I have buyers who are now kind of at a standstill,” said Yolanda Cortez, an L.A. area agent at Century 21 Realty Masters.

Some were already looking at homes in the L.A. area at the top end of their budget.

But after interest rates rose, Cortez said, they can now afford only a house in the Antelope or Victor valleys, high-desert communities more than 60 miles from downtown Los Angeles, a nonstarter “because they work in the L.A. area.”

As a result, fewer homes are going into escrow, inventory is rising and sellers are starting to react.

The share of homes listed for sale that took recent price cuts has more than doubled since last year. During the four weeks that ended June 5, 16.2% of listings in L.A. County had at least one price cut, up from 7.5% during the same period last year, Redfin data show.

In Orange, Riverside and San Bernardino counties the share of price drops rose to more than 20% of listings, up from about 7% a year earlier.

Nationwide, there haven’t been this many price cuts since 2019. Homes for sale in Los Angeles and Orange Counties haven’t seen this number of price reductions since late 2018 — the last time mortgage rates shot up. In the Inland Empire, price reductions are at an all-time high in a dataset that started in 2015.

Despite the slowdown, agents say that there are still many eager buyers and that the number of homes for sale remains well below pre-pandemic levels, with bidding wars still breaking out for the best properties.

Tregg Rustad, an agent at Rodeo Realty, said that two weeks ago his client submitted an offer on a Silver Lake house that was hundreds of thousands of dollars above the asking price.

“The buyer didn’t get it,” he said, noting he’s seen similar bidding wars in Santa Monica and Hancock Park.

Still, there has been a marked shift in the environment for would-be home buyers, and other changes are afoot as price cuts become more common.

In the last two years, many sellers ignored offers unless buyers waived certain contingencies, particularly the appraisal contingency that allows a buyer to walk away if an appraisal comes in low.

Now, buyers can leave those contingencies in place and have their offers taken seriously, said real estate agent Derek Oie, founder of Movement Real Estate in the Inland Empire.

Buyers “are not in the driver’s seat,” Oie said. “But they are not being dictated to anymore.”

Carl Izbicki, a real estate agent at RE/MAX Estate Properties in Los Angeles, said homes that used to get about 15 to 25 offers now get three to five.

When the market was on fire, one of Izbicki’s clients, a couple, lost out on about eight homes despite bidding well above the asking price. Last week, Izbicki sent them a list of properties that have been on the market for more than 30 days.

“If they like one of these homes, we are going to offer less,” he said.

In an interview a few days later, Izbicki said the couple did just that, offering about $40,000 less than the asking price on a three-bedroom home in Van Nuys listed at $789,000. They are waiting to hear back.

Michael Simonsen, founder of real estate data firm Altos Research, said that though some buyers are now priced out, others probably have paused their searches for other reasons.

As inventory rises, even those who can still buy are choosing not to, creating somewhat of a self-fulfilling slowdown prophecy.

“Buyers know they can wait maybe until the summer and have more selection,” Simonsen said.

Despite the increased prevalence of price cuts, many analysts don’t predict the actual value of Southern California homes to fall soon — absent a recession.

After accounting for price reductions, most sellers are still listing their homes at higher prices than a year ago, and on average, homes are still selling for above the list price, said Taylor Marr, a Redfin economist.

In Los Angeles County, the initial median list price — the price at first listing — for the four weeks that ended June 5 was 9% higher than it was in the same period last year, while the average price drop — which occurs on a growing but still minority number of listings — was 5%, according to Redfin.

Experts said some of the recent price cuts probably came from overeager sellers who priced their properties way over market value to take advantage of what until recently was a very hot market.

Further guarding against value declines, homeowners who don’t need to sell may choose not to in a softening market.

Izbicki, for example, just dropped the price on a two-bedroom condo in Palms by $24,000. If no one offers close to the new list price of $824,000, he said his client plans to rent it out instead.

Many analysts predict home prices will keep rising this year, but by a smaller percentage than they are rising now.

One of the more downbeat forecasts comes from John Burns Real Estate Consulting, which last month predicted that by December 2022, Southern California home prices will have risen by the mid-single digits compared with a year earlier, a marked slowdown from the roughly 20% gain in May.

The consulting firm predicted home prices would then decline by the mid-single digits in both 2023 and 2024 as the Fed’s efforts to fight inflation push the economy into recession.

The market may morph further, however. After a report Friday that showed inflation accelerated, more economists now expect the Federal Reserve this week will raise interest rates by more than what had been widely expected, which could send mortgage rates even higher.

On Monday, partly in anticipation of a more aggressive Fed, the average rate on a 30-year mortgage hit 6.18%, up from 5.5% the previous Monday, according to Mortgage News Daily.

Rick Palacios Jr., director of research at John Burns Real Estate Consulting, said the research firm is debating whether to adjust its forecast downward because of the jump by mortgage rates above 6%.

Already, “there are not a ton of buyers,” said Heather Presha, a Keller Williams agent who specializes in South L.A. “I wouldn’t be surprised that by the end of the year we are kind of midway to a buyer’s market.”

The Times produced a guide to help first-time home buyers navigate the market. Check out the Great SoCal House Hunt here. An abridged print version is available for purchase here.